Case Study: The Pre-Tax Winner That Loses After Tax

This case study compares a high-turnover rule-driven portfolio with a lower-turnover benchmark for a single New York resident earning $200,000.

Open Portfolio Backtest →The Goal

This example asks whether a high-turnover rule-driven strategy belongs in a taxable brokerage account. The comparison target is after-tax ending wealth, not only pre-tax return.

We compare two portfolios from 2010-01-04 through 2025-12-31 with a $10,000 starting principal:

| Portfolio | Construction | Role In Comparison |

|---|---|---|

| Rule-Driven Tax Magnet | 70% UPRO/SHY rule-driven strategy + 20% SPY + 10% AGG | High-turnover taxable portfolio under test. |

| Benchmark 80/20 | 80% SPY + 20% AGG | Lower-turnover comparison portfolio. |

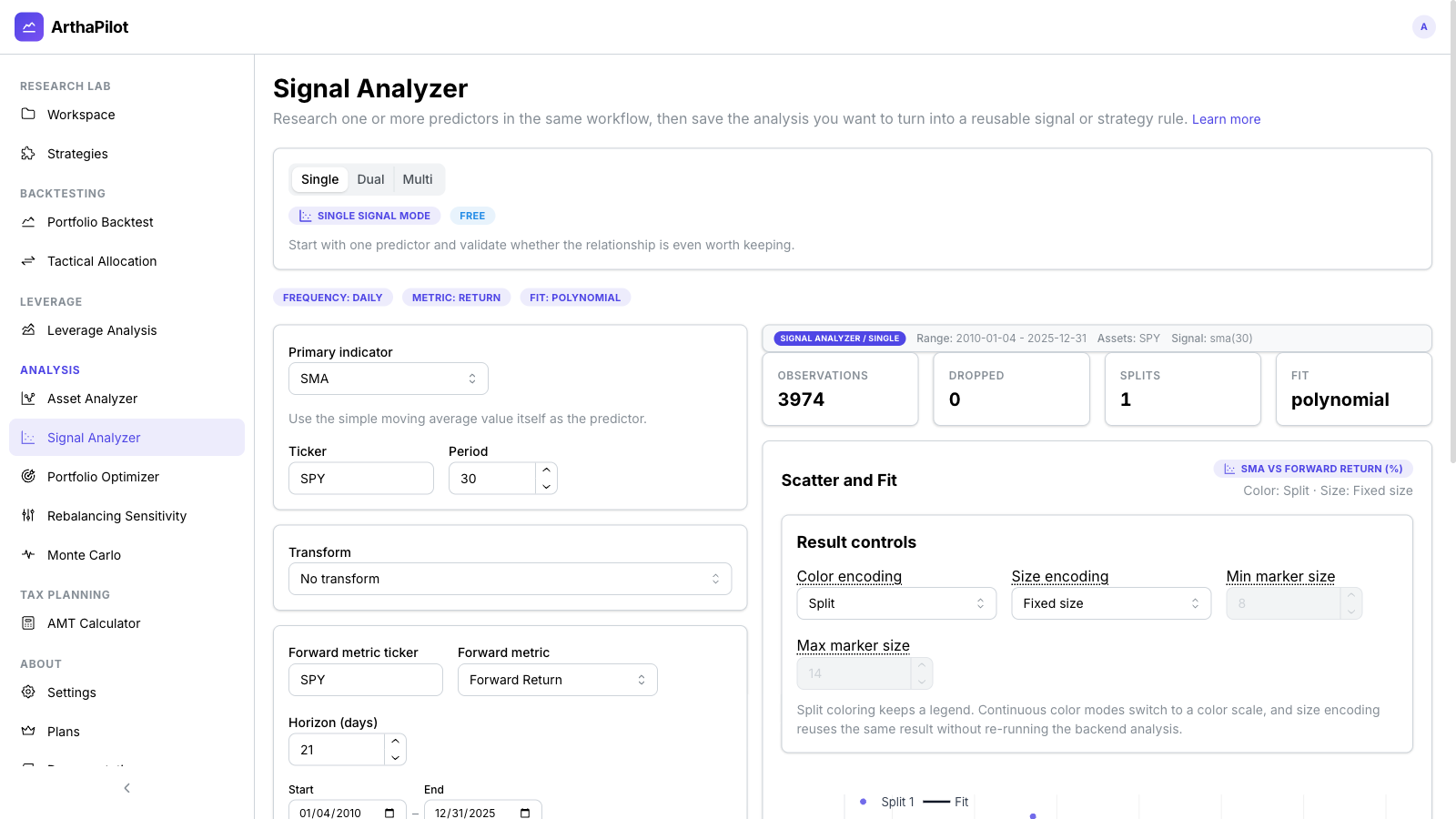

Step 1: Validate The Predictor In Signal Analyzer

Start in Signal Analyzer. The Strategy Builder rule uses one predictor: whether SPY is above or below its 30-day simple moving average (SMA). The goal is to check whether the indicator has a measurable relationship with a later outcome before turning it into a trading rule.

- Target: SPY forward 21-day return

- Indicator: SPY 30-day SMA

- Purpose: measure whether the signal separates forward returns before introducing leverage and turnover

Step 2: Build The Strategy

Use Strategy Builder to implement a two-state rule:

- Risk-On: 100% UPRO when SPY is above its 30-day simple moving average

- Risk-Off: 100% SHY as the fallback state

- Trading frequency: Daily

- Benchmark: SPY

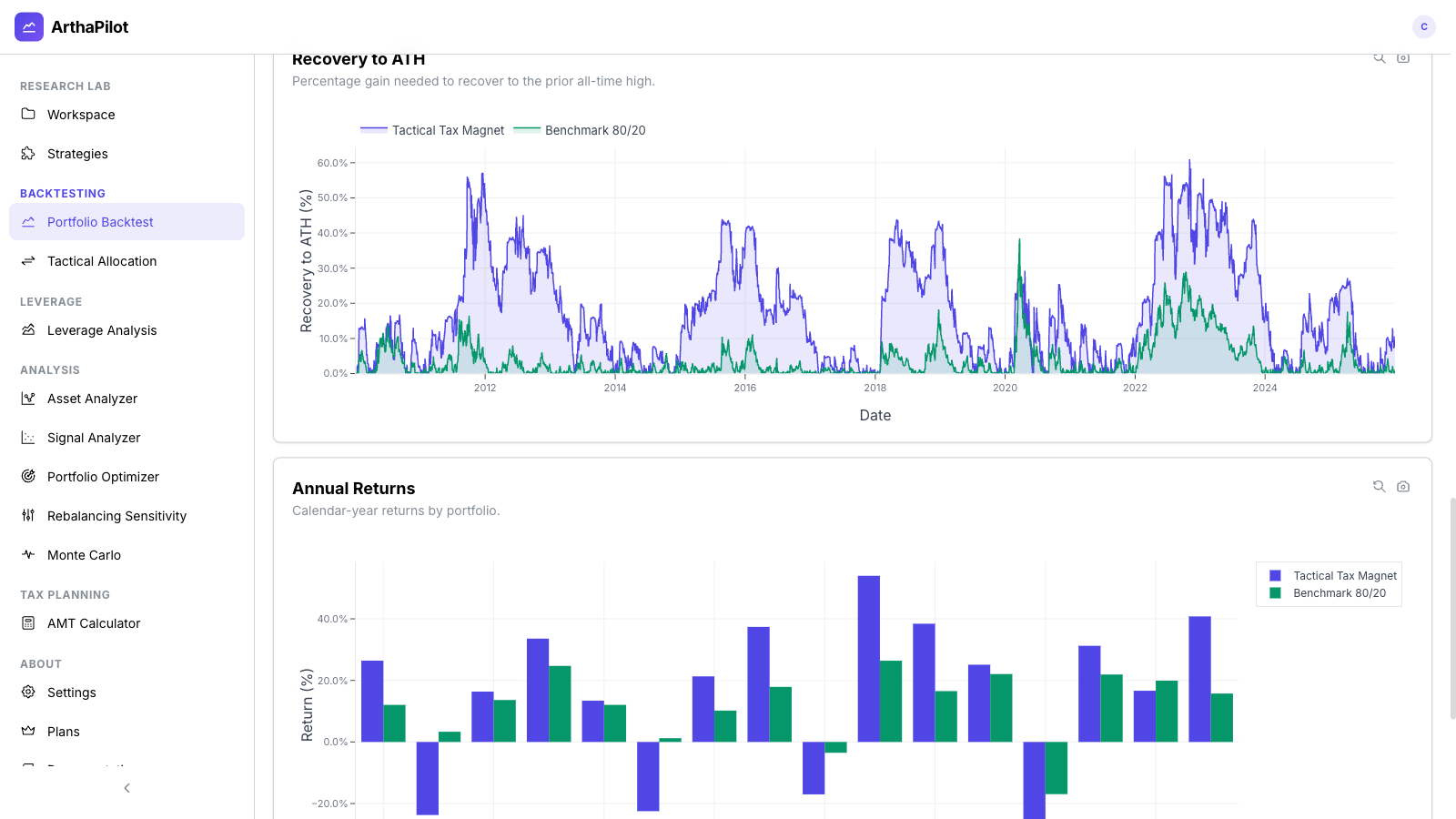

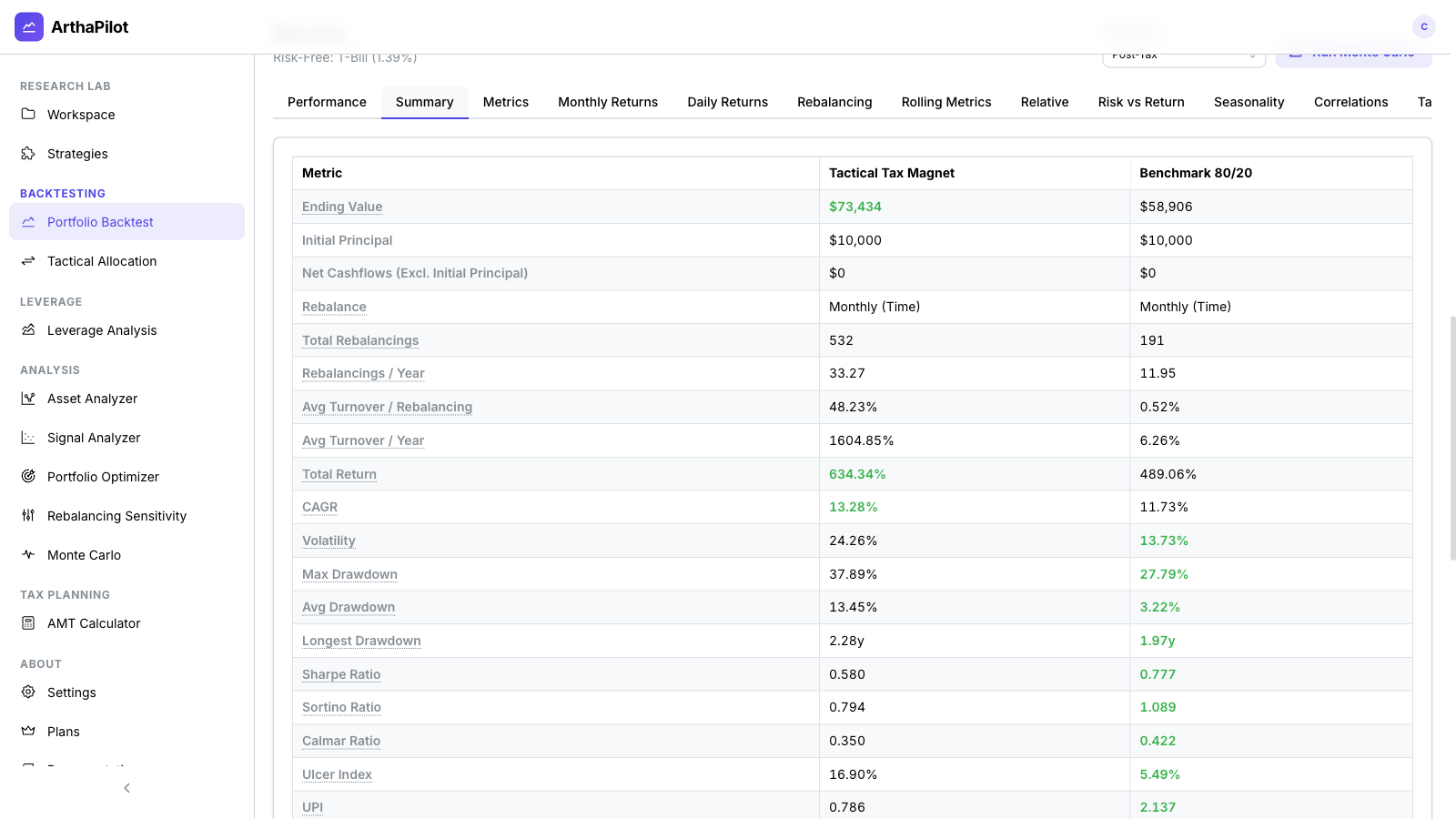

Step 3: Run The Pre-Tax Portfolio Backtest

Compare this portfolio with a benchmark in Portfolio Backtest using Price Mode = Total Return and monthly portfolio rebalancing. On this first pass, the rule-driven portfolio has the higher ending value and higher CAGR.

| Metric | Rule-Driven Tax Magnet | Benchmark 80/20 |

|---|---|---|

| Ending Value | $73,434 | $58,906 |

| CAGR | 13.28% | 11.73% |

| Sharpe Ratio | 0.580 | 0.777 |

| Max Drawdown | 37.89% | 27.79% |

Step 4: Turn On The Tax Profile

Next, enable Tax-Aware mode and model the investor:

- Filing status: Single

- Annual income: $200,000

- Resident state: New York

- Lot selection: Optimized

- Account type: Taxable Brokerage

Step 5: Compare The After-Tax Result

The Tax Analysis tab plots pre-tax and after-tax value for each portfolio and summarizes the after-tax outcome:

| After-tax outcome | Rule-Driven Tax Magnet | Benchmark 80/20 |

|---|---|---|

| After-Tax Ending Value | $31,440 | $52,585 |

| After-Tax CAGR | 7.43% | 10.94% |

| Tax Drag (Annualized) | 7.38% | 0.80% |

| Total Taxes Paid | $28,626 | $3,089 |

In this run, the portfolio with the higher pre-tax ending value leaves the investor with about $21,000 less after tax.

Step 6: Inspect The Cause

The summary tables show why the ranking changes:

- The rule-driven portfolio executed 532 rebalances, versus 191 for the benchmark.

- Average turnover per year was 1604.85%, versus 6.26% for the benchmark.

- The tax summary shows $120,502 of short-term gains and $163,499 of wash-sale-disallowed losses for the rule-driven portfolio.

- The benchmark pays less tax because it trades less and realizes far fewer short-term gains.

Step 7: Check Rebalancing Comparison

After the ranking flips, the next question is whether the result is sensitive to one rebalance schedule. Move to Rebalancing Comparison and compare frequencies and offsets for the lower-turnover candidate.

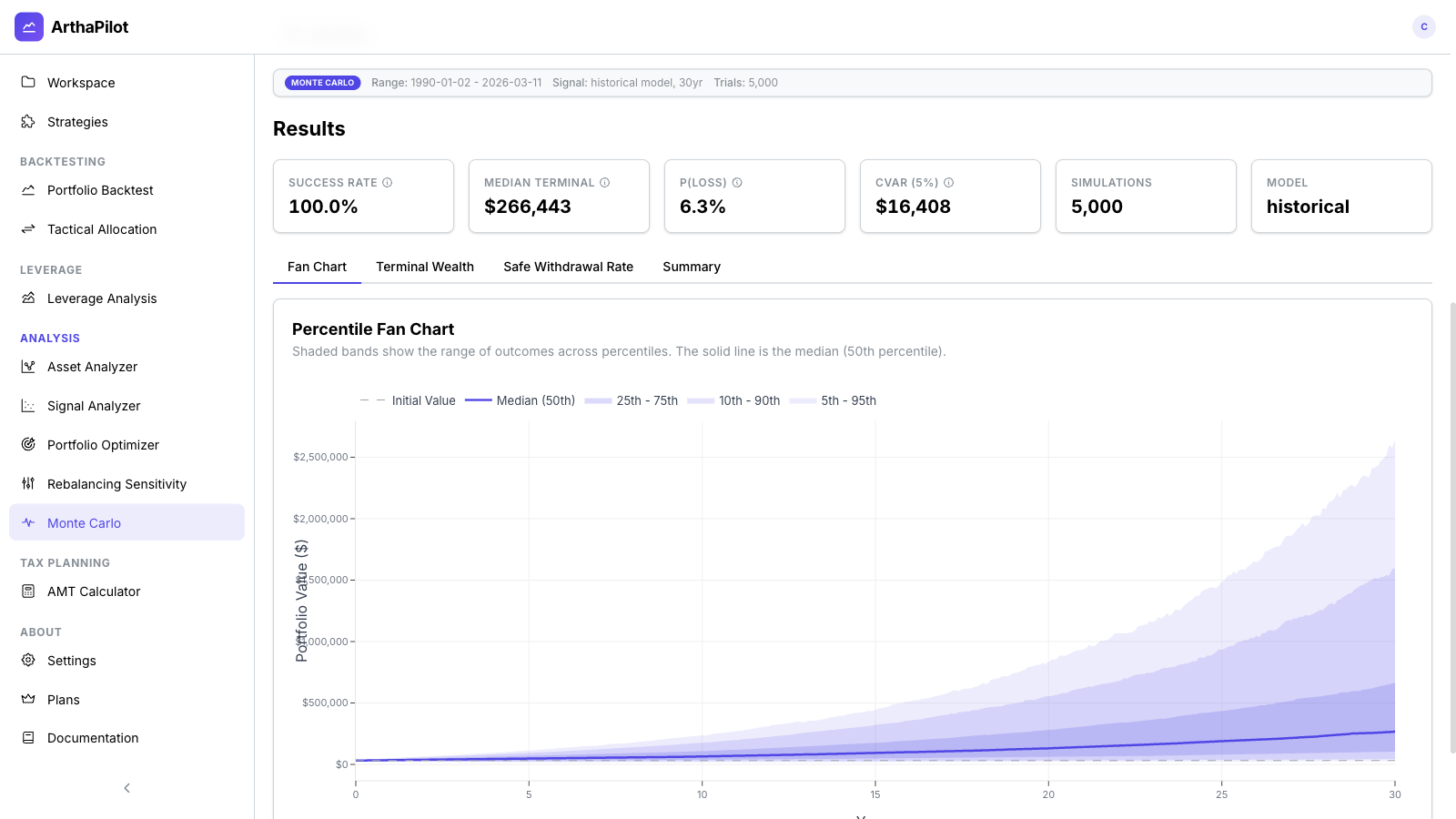

Step 8: Run Monte Carlo On The Surviving Portfolio

Use Monte Carlo to inspect the forward distribution of the lower-turnover portfolio.

Key Takeaways

- A pre-tax winner can lose after tax.

- Turnover, short-term gains, and wash-sale effects can dominate the gross return advantage of a taxable rule-driven strategy.

- The relevant comparison is the investor's after-tax outcome, not only the pre-tax equity curve.